By Tracey Panek

Trade Credit Content Marketing Manager

Dun & Bradstreet

November 5, 2018

How to Make Business Credit Applications for New Customers

What’s the process for when a new customer applies for business credit at your company? Do you email them a PDF of your credit application with instructions to fill it out, sign it, scan it, and send it back?

Do you wish there were a better way?

As many companies consider digital workflows to eliminate paper-based processes, applications for business credit are getting a second look. While some companies still rely on fax machines to accept hand-signed applications and some accept emailed attachments, the companies that really want to improve their business processes are implementing online business credit applications.

Much has already been written about the benefits of creating an online credit application form : how such forms make it easier for your customers to place orders, get approved, and do business with you in general, and how they decrease turnaround times and reduce errors for credit teams. And if your company operates in a high-volume industry, an online credit application is almost a necessity.

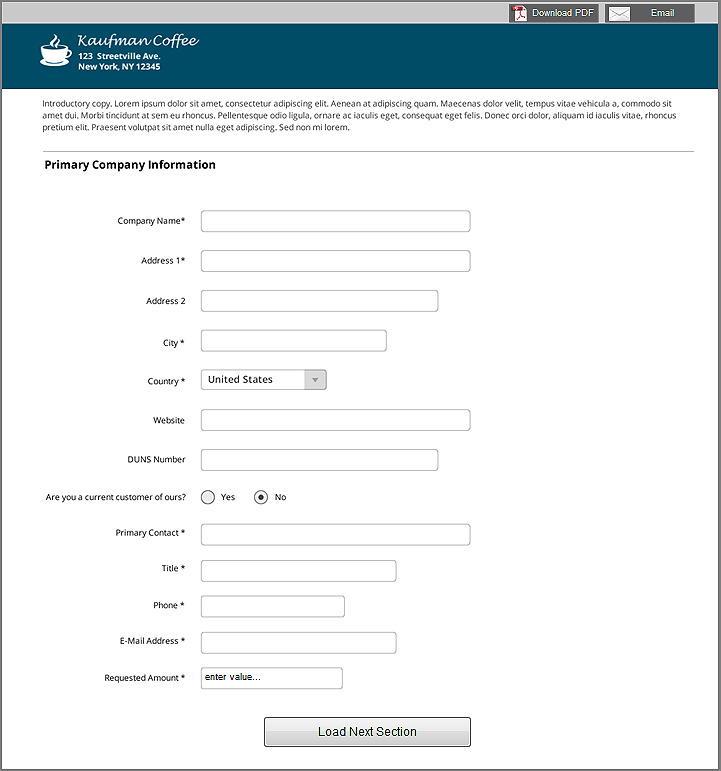

Yet companies that are undergoing such digital transformation initiatives may be so focused on the technology aspect of implementation that they forget about what’s actually in the credit application template. If and when your company is going through the process of allowing customers to submit the application online, it’s also a great time to review and reassess the application’s form fields. You want to make sure you’re capturing all the data you need to make an informed business credit decision and provide the best possible terms. Consider that you’ve probably had years of collecting this information via paper-based applications: Where have you been successful, and what fields did your customers often leave blank?