The Global Risk Matrix Q3 2018

Ten Key Global Risks for Businesses

The Dun & Bradstreet Global Risk Matrix (GRM) ranks the biggest threats to business based on each risk scenario’s potential impact on companies, assigning a score to each risk. The scores from the top ten risks are used to calculate an overall Global Business Impact (GBI) score.

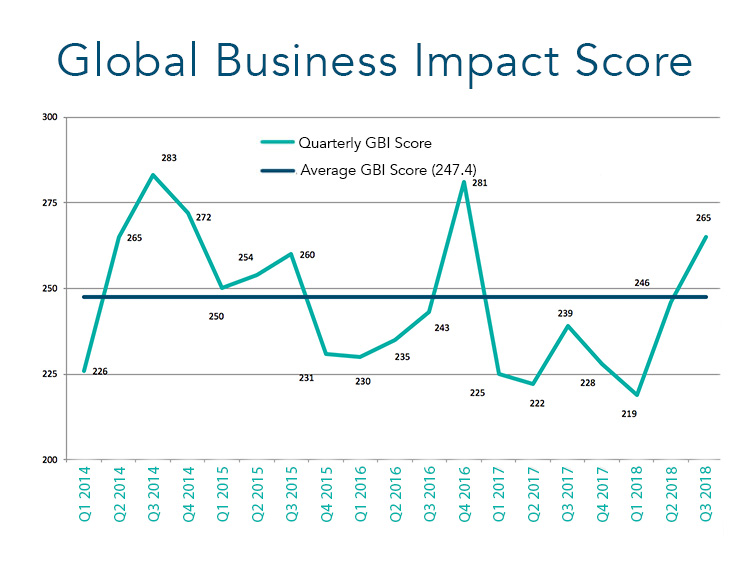

Our latest GBI score highlights a second successive worsening in outlook for cross-border businesses, taking risk to its highest level since Q4 2016. The score is also above the long-term average for the first time since that quarter.

International Trade Risks Worsen for Second Consecutive Quarter

Overall, risks remain geographically spread and diverse, associated with trade wars, politics, economic developments, new technology, and climate change.

Dun & Bradstreet’s GBI score worsened significantly for a second successive quarter, increasing from 246 (out of a maximum 1,000) in Q2 2018 to 265 in Q3, indicating a deterioration in the global business operating environment. The Q3 score is the highest since the politically-induced spike of Q4 2016 and is well above both the long-term average (246.4) and the 2017 average (228.5). It also shows that there has been a significant worsening in business risk through 2018 since the record low of 219 seen in the first quarter.

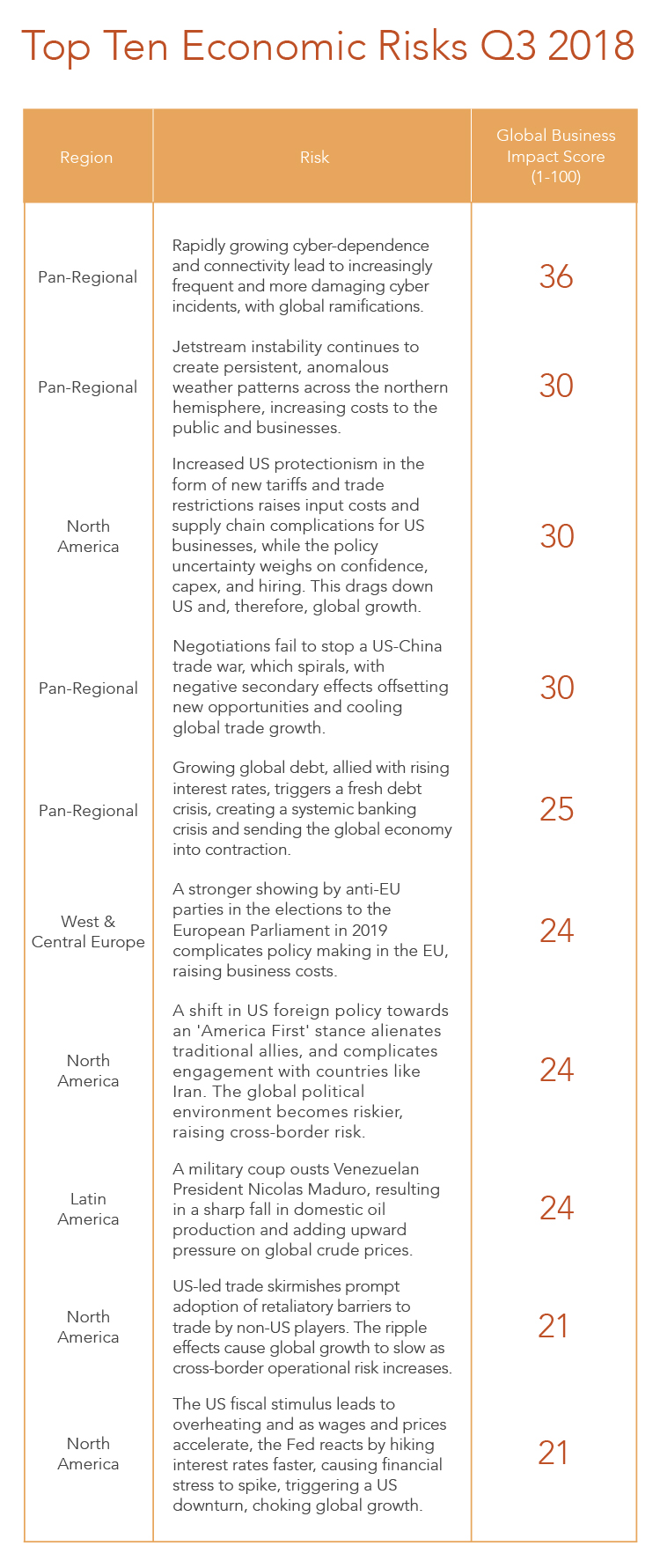

Our top ten risks combine an assessment of: (i) the magnitude of the event’s probable effect on the global business operating environment, on a scale of 1 to 5 (where 1 is the smallest impact and 5 is the largest); and (ii) the likelihood of the event happening.

Six New Risks in the Global Top Ten

Highlighting the rapidly changing global environment, there are six new entries in Dun & Bradstreet’s Q3 2018 Global Risk Matrix: three from North America, one each from Western and Central Europe, and Latin America, as well as one pan-regional risk.

The six new-entry risks are:

-

Jetstream instability continues to create persistent, anomalous weather patterns across the northern hemisphere, increasing costs to the public and businesses (GBI 30, out of a maximum 100)

-

Increased US protectionism in the form of new tariffs and trade restrictions raises input costs and supply chain complications for US businesses, while policy uncertainty weighs on confidence, capex, and hiring. This drags down US (and therefore global) growth (GBI of 30)

-

A stronger showing by anti-EU parties in the elections to the European Parliament in 2019 complicates policy making in the EU, increasing business costs (GBI of 24)

-

The shift in US foreign policy towards an ‘America First’ stance alienates traditional allies and complicates engagement with countries such as Iran. As a result, the global political environment becomes riskier, raising cross-border risk for businesses (GBI of 24)

-

A military coup ousts Venezuela’s President Nicolas Maduro, resulting in a sharp fall in domestic oil production and adding upward pressure on global crude prices (GBI of 24)

-

US-led trade skirmishes prompt adoption of retaliatory barriers to trade by non-US players. The ripple effects cause global growth to slow as cross-border operational risk increases (GBI of 21)

Among our pre-existing risks, two are unchanged, while one GBI score has deteriorated and one has improved. Overall, risks remain geographically spread and diverse, associated with trade wars, politics, economic developments, new technology, and climate change. This reinforces the fact that finance, procurement and supply chain teams across all business sectors have to combat the impacts of an increasingly complex and globalised world.

‘America First’ Risks are Significant

Our Q3 2018 Global Risk Matrix indicates that the impact of Washington’s ‘America First’ policy is reverberating across the globe, raising risk for doing cross-border business; four of our top ten risks are associated with this policy. In equal second place, with a GBI of 30, is the risk that increased US protectionism in the form of new tariffs and trade restrictions raises input costs and supply chain complications for US businesses, while the resultant policy uncertainty weighs on confidence, capex, and hiring. This will impact on US growth and, therefore, global growth. Also in equal second place, with a GBI of 30 (up from 21 in the previous GRM), is our concern that US-China trade negotiations fail to stop a trade war, which spirals, with negative secondary effects offsetting new opportunities and cooling global trade growth.

The third risk associated with America First is in equal sixth place, with a GBI of 24. This relates to the foreign policy impacts of the policy, in the event that they alienate traditional allies and also raise tensions with countries such as Iran and Venezuela – this would raise risks for doing cross-border business globally. In equal ninth place, with a GBI of 21, is the final America First risk, which is the wider issue of trade wars prompting the raising of trade barriers by the likes of the EU, Asia-Pacific and Latin American countries, increasing risks and costs for cross-border business.

Additional Political Risk Factors

In equal sixth place, with a GBI of 24, is the risk associated with 2019’s European Parliamentary elections in the EU, which could see a stronger showing by anti-EU parties. This would complicate policy-making in the bloc, raising barriers to intra-EU commercial activity. In addition, in Latin America, we worry that a military coup against Venezuela’s President Nicolas Maduro could lead to a sharp fall in domestic oil production, triggering oil prices over USD90/b. This risk is in equal ninth place, with a GBI of 21.

Economic Risk Factors

Two economic concerns feature in this quarter’s GRM. In fifth place with a GBI of 25 (the same score as the previous report) is the pan-regional concern that growing global debt, allied to rising interest rates, will trigger a fresh debt crunch, creating a systemic banking crisis and sending the global economy into contraction. Meanwhile, in equal ninth place with a GBI of 21 (down from first place with a GBI of 40 in the previous GRM) is a threat emanating from North America. We are worried that US fiscal stimulus leads to an overheating of the US economy, heralding a consequent slowdown which would, in turn, impact global economic growth.

Other Factors

The final two factors are both pan-regional and occupy the top two spots in the matrix. In first place with a GBI of 36 (the same as the previous report) is our concern that the rapidly growing problem of cyber-dependence and connectivity will lead to more frequent and more damaging cyber-security issues, with ramifications for doing business; this risk has become increasingly evident in recent quarters. In second place overall, with a GBI of 30, is a risk associated with climate change. Specifically, we are concerned that jetstream instability continues to create persistent, anomalous weather patterns across the northern hemisphere, increasing costs to the public and businesses.

Summary: Business Environment Deteriorates Sharply Again

The Dun & Bradstreet Global Business Impact score for Q3 2018 shows that risks facing businesses have worsened for a second consecutive quarter (following the record low score recorded in Q1 2018). The Q3 score highlights that, despite the embedding of the global economic recovery, business decision-makers need to monitor the global business environment continually and carefully. The geographical spread and diversity of risks around trade wars, politics, economic developments, new technology, and climate change ensure the business environment remains challenging.